FEMA’s New 50% Cost-Share Policy: Implications for States and Insurers in 2025

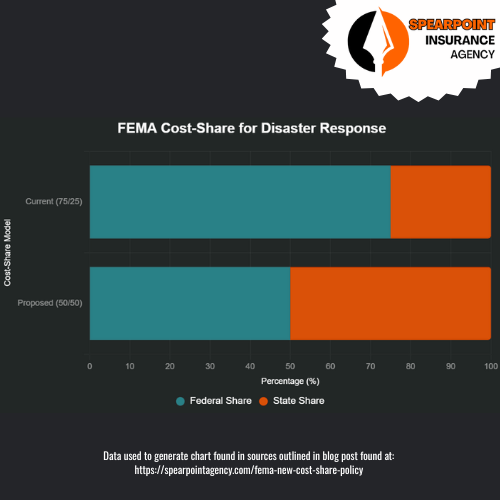

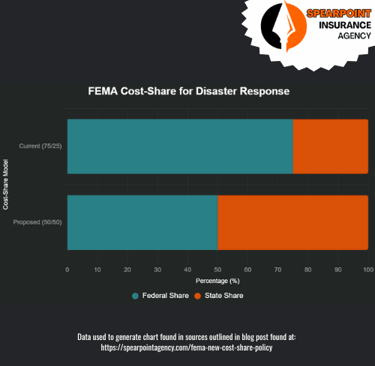

The Federal Emergency Management Agency (FEMA) is set to undergo significant changes in 2025, with a new policy that will shift more financial responsibility for disaster response to states. According to an Insurance Journal article published on May 15, 2025, FEMA’s new chief, David Richardson, announced that states will soon bear 50% of the costs for responding to natural disasters, up from the current 25% cost-sharing level. Let’s explore the details and what this means for stakeholders.

FEMA’s Cost-Share Reform: A Vision for Efficiency

Under the leadership of David Richardson, a former Marine artillery officer appointed just a week before the announcement, FEMA is embracing a bold new direction. The Insurance Journal reports that Richardson plans to align FEMA’s operations strictly with its legal mandates, reducing federal overreach and shifting more responsibility to states. The proposed 50/50 cost-share model for disaster response, set to take effect as early as 2026, will require states to cover half the costs, compared to the current 75/25 federal-state split. “FEMA 2 will look different than FEMA 1,” Richardson declared at a staff town hall, emphasizing state-led response, recovery, and preparedness.

This policy reflects conservative principles of limited government and fiscal discipline. By reducing federal spending on disaster response, the Trump administration is empowering states to take charge, encouraging them to develop robust, self-sufficient emergency management systems. Richardson has advised FEMA staff to alert governors to this shift, ensuring transparency and giving states time to prepare. While some states may receive additional federal support in extreme cases, this reform promotes accountability and reduces reliance on Washington.

Leadership Driving Insurance Industry Progress

The government is taking decisive steps to bolster the insurance industry, recognizing its critical role in economic stability. The FEMA cost-share reform is part of a broader agenda to create a more efficient, market-driven environment for insurers. Department of Homeland Security Secretary Kristi Noem and President Donald Trump have pushed for FEMA’s restructuring, rejecting the status quo of bloated federal programs. This aligns with their broader vision to cut bureaucratic red tape, as evidenced by Richardson’s replacement of former acting chief Cameron Hamilton, who was ousted after opposing agency reforms.

These efforts are already fostering a more competitive insurance market. By encouraging states to shoulder more disaster response costs, the administration is incentivizing insurers to innovate. For example, companies like Kentucky Growers Insurance are adopting advanced platforms like the Finys Suite to streamline operations, reflecting a market response to the need for efficiency. Similarly, global trends, such as OP Financial Group’s partnership with Accenture to modernize its non-life insurance division, show how the industry is adapting to a changing landscape—one that government policies are helping to shape by prioritizing local control and private-sector innovation.

Addressing Rising CosTS

As states adjust to the new FEMA policy, potential increases in disaster-related costs could impact insurance premiums, particularly in high-risk areas. The Insurance Journal notes that economic pressures, such as proposed automotive tariffs highlighted by Progressive Corporation in April 2025, may drive up car insurance costs through 2026. Additionally, climate-driven events like the 2025 California wildfires have led to rate hikes, with State Farm approved for a 17% increase. These challenges underscore the need for solutions that protect consumers while maintaining market stability.

Enter Spearpoint, a forward-thinking insurance agency dedicated to helping policyholders navigate rising costs. Spearpoint offers innovative tools and services, including AI-driven risk assessment and personalized policy options, to help consumers find affordable coverage tailored to their needs. By leveraging data analytics, Spearpoint enables insurers to offer competitive premiums, even in high-risk regions (like Florida), mitigating the financial impact of state-level cost increases. For example, Spearpoint’s platform can help homeowners in hurricane-prone states secure cost-effective policies, aligning with the emphasis on market-driven solutions over government handouts.

A Resilient Future

The Insurance Journal article highlights a pivotal moment for disaster response and the insurance industry. FEMA’s 50% cost-share policy, driven by conservative leadership, is set to empower states, reduce federal spending, and foster a more resilient national framework. Meanwhile, companies like Spearpoint are stepping up to ensure that rising costs don’t burden consumers, offering innovative solutions that complement the administration’s vision for a leaner, more efficient system.

For more details on FEMA’s reforms, read the full Insurance Journal article at https://www.insurancejournal.com/news/national/2025/05/15/823980.htm.

As government policies drive progress and change amongst the insurance market, Spearpoint is here to help you navigate all of your insurance needs. Reach out to one of our licensed insurance experts today to discuss your options!

Spearpoint Insurance Agency, Inc.

NPN: 20316334

CALL NOW:

Fax: +1-586-221-6750

© 2022-2026 by Spearpoint Insurance Agency, Inc.

Mailing Addresses:

4200 Fashion Square Blvd. Ste. 201

Saginaw, MI 48603

8270 Woodland Center Blvd

Tampa, FL 33614

quote@spearpoint.info

Licensed In The Following States:

If you do not see your state above, please send us a message. Thank you!